Live The Adventure

We respectfully acknowledge that we are on the traditional territory of the Kwakiutl people, Gilakas’la

what's happening in Port Hardy

April 24, 2024

The District is pleased to announce Naomi Heith’s appointment as the new Manager of Recreation and Community Services. With a wealth of experience and...

what's happening in Port Hardy

April 08, 2024

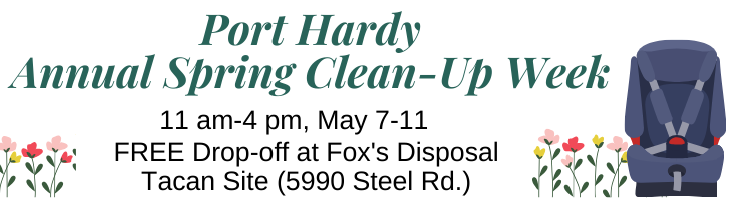

It’s that time of year again! Port Hardy’s Annual Spring Clean-Up Event is scheduled to take place 11 AM-4 PM, May 7- 11. Port...

what's happening in Port Hardy

March 14, 2024

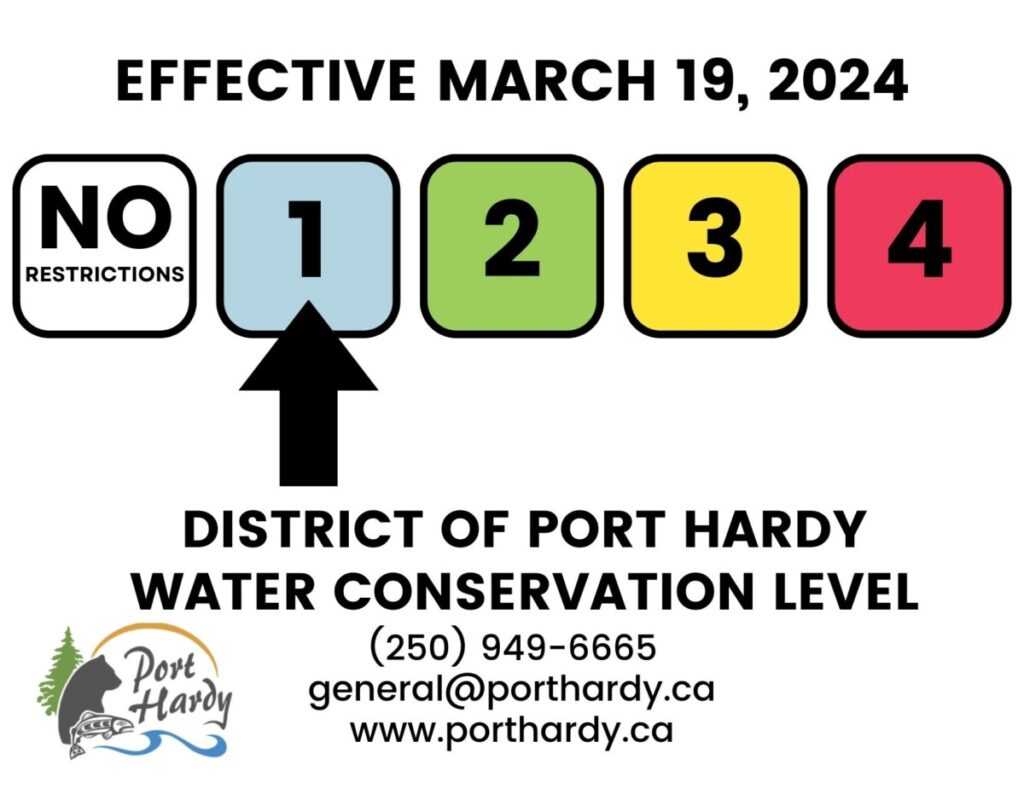

As of March 19, 2024, the District of Port Hardy will move to Level 1 Water Conservation Stage. While annual water conservation measures typically...

what's happening in Port Hardy

February 28, 2024

The last few weeks have been a horrible time for our town and the surrounding communities, and the deaths weigh heavily on myself, the...

what's happening in Port Hardy

February 13, 2024

The District of Port Hardy is pleased to announce the launch of the Situation Table, a groundbreaking initiative to provide comprehensive support to individuals...

what's happening in Port Hardy

September 29, 2023

During an emergency, Emergency Support Services (ESS) volunteers work closely with impacted residents to connect them with needed services including accommodations, food, and incidentals....

what's happening in Port Hardy

June 21, 2023

Did you miss the Session, listen here SAFER PLACE TO BE PROJECT EVALUATION 2022 SEPT 27 FINAL SAFER PLACE TO BE PROJECT EVALUATION...

what's happening in Port Hardy

November 30, 2022

The North Island Crisis & Counselling Centre and the RCMP are pleased to announce the launch of Third Party Reporting in the North Island....

what's happening in Port Hardy

April 29, 2022

We are excited to announce the Adopt-A-Street program! By signing up, participants will volunteer to clean a street in Port Hardy twice monthly,...

what's happening in Port Hardy

December 02, 2019

The District launched the Mass Notification System in 2018 which will alert subscribers via land line, cell phone, text message and email of important...

what's happening in Port Hardy

what's happening in Port Hardy

May 08, 2024

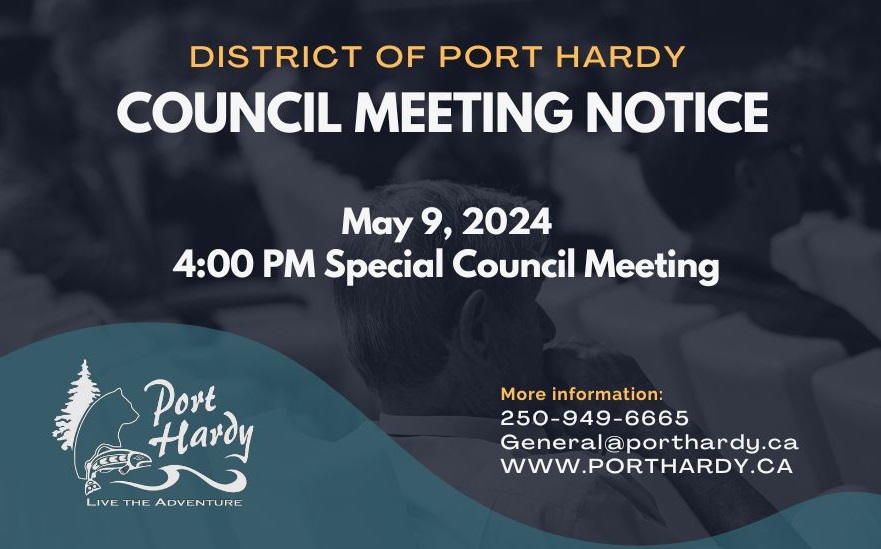

Join Mayor and Council tomorrow, Thursday, May 9 at 4:00 pm for the presentation of 2023 Draft Financial Statements and Audit Findings Report. Join...

what's happening in Port Hardy

May 06, 2024

Water service will be temporarily interrupted to all residential and commercial properties located in the service areas shown in notice, to complete repairs to...

what's happening in Port Hardy

May 06, 2024

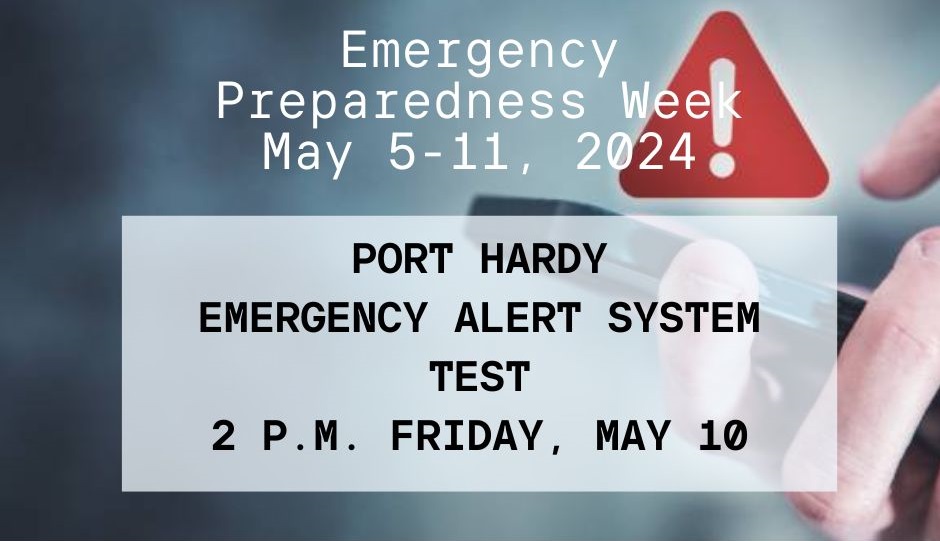

As part of Emergency Preparedness Week, the District of Port Hardy will issue a TEST emergency alert at 2 P.M. on Friday, May 10,...

what's happening in Port Hardy

May 01, 2024

May is GBS/CIDP Awareness Month. Guillain-Barré Syndrome is an inflammatory disorder of the peripheral nerves outside the brain and spinal cord. Chronic Inflammatory Demyelinating...

what's happening in Port Hardy

April 26, 2024

Check out the Spring 2024 for an update on the current watering restrictions, more information on the Annual Spring Clean-Up Week, and how prepare...

visit Port Hardy

meeting portal

Stay up to date on the latest Council and Committee meetings